Last Updated on 2 months ago by The Executive post

Most Indians have no emergency fund. A SEBI Investor Survey found that nearly 76% of households could not handle a financial shock lasting more than three months. One unexpected hospital bill, one pink slip, one broken-down car — and suddenly you’re borrowing from family or maxing out a credit card at 40% interest.

If you lost your salary tomorrow, how long could you survive without borrowing?

By the end of this article, you’ll know exactly how much to set aside, where to park that money in India for the best mix of safety and returns, and the most common mistakes people make — so you can avoid repeating them.

Table of Contents

What Is an Emergency Fund and Why Do You Actually Need One

An emergency fund is a fixed pool of money that you set aside in a completely liquid and easily accessible account, meant only for genuine financial emergencies. It is the cash you rely on when life throws unexpected challenges your way — whether it’s a sudden job loss, a medical crisis, major home repairs, or an urgent family obligation that simply cannot wait.

It is not your “I’ll invest it someday” money. It is not the fixed deposit you’ll “break only if needed.” It is purpose-built cash that does one job: keep you financially stable when life goes sideways.

Here’s why this matters more in India than most financial content admits. India does not have a robust social safety net the way the UK or parts of Europe do. There is no universal unemployment benefit you can fall back on if you’re laid off from a private company. Employer-provided health insurance almost always ends on your last working day — and private hospital bills in tier‑1 cities can easily hit ₹2–5 lakh within a week of admission.

Let’s be honest: even salaried professionals with decent incomes are one bad month away from financial stress if they carry large EMIs and have no buffer.

Without an emergency fund, your only options in a crisis are: breaking your long-term investments — mutual funds, PPF, stocks — often at exactly the wrong moment when markets are down; or taking a personal loan at 14–24% interest, which compounds your financial problems on top of whatever emergency you’re already dealing with.

Your emergency fund is what separates a temporary financial setback from a long-term financial disaster. It protects your investments. It keeps your credit score intact. It gives you time to make rational decisions instead of panicked ones.

And here’s the practical part: Tracking expenses apps can play a role here too. The best ones don’t just categorize your daily spending, they also let you earmark contributions toward your emergency fund. When you see that line item grow month after month, it’s a reminder that you’re building resilience, not just tracking groceries and EMIs.

The rule every financial planner agrees on: build your emergency fund before you start investing in anything else before mutual funds, before stocks, before cryptocurrency, before anything. And if your expense tracker helps you stay disciplined, that’s one app feature worth paying attention to.

How much should be Emergency Fund in India

This is where most advice gets frustratingly vague. “Save 3 to 6 months of expenses” — fine, but what does that actually mean for a 32-year-old in Pune with two kids and a home loan?

Let’s break it down properly.

The formula is simple: multiply your total monthly expenses by 3, 4, or 6 depending on your risk profile. Use your actual monthly expenses — not your salary. Include rent or home loan EMI, groceries, school fees, utilities, internet, phone bills, insurance premiums, medicine, and any other fixed costs. Exclude discretionary spending like eating out, entertainment, and shopping, since those are the first things you’ll cut in a real emergency.

How to pick your multiplier:

- 3 months — if you’re a government employee or work at a large MNC, have a working spouse, and your household has two income sources

- 4–5 months — if you’re salaried at a mid-size private company, are the primary breadwinner, or have one parent financially dependent on you

- 6 months — if you’re a freelancer, consultant, or self-employed; if you work at a startup; if you’re in a volatile industry like media, real estate, or manufacturing; or if you’re a single-income family

One more thing people overlook: if any family member has a chronic medical condition — diabetes, a heart condition, a dependent child with special needs — add one to two extra months on top of your base target. Healthcare emergencies in India escalate fast and hit without warning.

Here’s what the numbers look like in practice:

| Profile | Monthly Expense | Multiplier | Target Fund |

| Salaried, dual income, Bengaluru | ₹60,000 | 3× | ₹1,80,000 |

| Freelancer, single income, Delhi | ₹45,000 | 6× | ₹2,70,000 |

| Business owner, family of 4, Chennai | ₹90,000 | 6× | ₹5,40,000 |

One important point: if you’re just starting out, don’t let the final number intimidate you. Start with a goal of ₹50,000 or one month of expenses. Even a small buffer changes how you respond to unexpected costs. Build from there.

Where to Keep Emergency Fund in India

Liquidity first. Returns second. Don’t lock it in a long-term FD or equity mutual fund — markets crash exactly when you need money most

| Option | Rate (2025) | Access | Best for |

| High-interest savings account | 3.5–7% p.a. | Instant | First ₹1–2 lakh |

| Liquid mutual funds | 6.5–7.5% p.a. | T+1 (next day) | Bulk of the fund |

| Sweep-in FD | 6.5–7.2% p.a. | Instant (auto-breaks) | Stable earners |

| Arbitrage funds | 6–7% p.a. | T+2, equity tax | ₹3 lakh+ amounts |

- Keep 1–2 months in high‑interest savings (IDFC First, AU Small Finance, YES Bank and others).

- Park remaining funds in a liquid fund.

- Avoid PSU savings accounts (SBI, PNB only 2.7–3%).

How to Build Your Emergency Fund— Step by Step

Reading about this is easy. Here’s what to actually do, starting today.

Step 1: Open a separate high-interest savings account. IDFC First Bank and AU Small Finance Bank both allow zero-balance accounts that you can open online in under 15 minutes. This is your dedicated emergency fund home.

Step 2: Calculate your target. Monthly expenses × your chosen multiplier. Write the number down somewhere visible.

Step 3: Set up an automatic transfer on your salary date — even ₹2,000 or ₹3,000 to start. Automation removes the willpower problem. If the transfer happens before you see the money, you won’t miss it.

Step 4: Direct any windfalls straight here. Tax refund from ITR filing? Goes here. Annual bonus? Goes here. Freelance payment? Goes here. Keep doing this until you hit the target.

Step 5: Once you have one month’s expenses saved, move anything beyond that into a liquid mutual fund for better returns. Keep just one month in the instant-access savings account.

Step 6: Define what counts as an emergency — before one happens. Write it down. A medical emergency: yes. Job loss: yes. A new phone: no. A last-minute trip: no. Having this defined means you won’t rationalize dipping in for the wrong reasons.

Most consistent savers reach their three-month target within 8–12 months. You’ll get there.

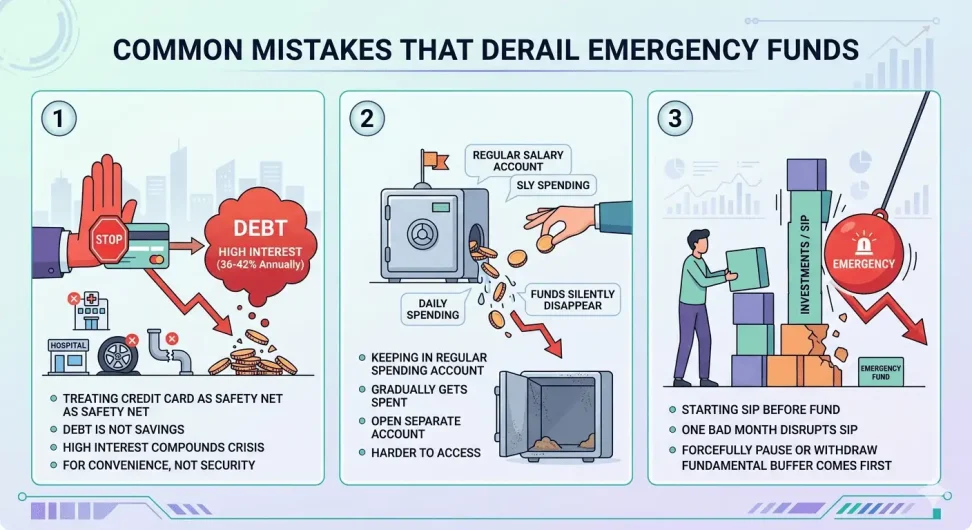

Common Mistakes That Derail Most People’s Emergency Funds

Most people understand the concept. Very few execute it right. Here are the mistakes that show up repeatedly.

Mistake 1: Treating your credit card limit as a safety net. A credit card is debt — not savings. If you use it during a crisis, you’re paying 36–42% annualised interest on that “emergency.” That compounds your problem, not solves it. A credit card is useful for convenience, not for financial security.

Mistake 2: Keeping it in the same account as your monthly spending. This is the single biggest reason emergency funds silently disappear. When the money is sitting in your regular salary account, it gets spent — slowly, a little every month. Open a separate account, ideally at a completely different bank. Out of sight, harder to spend.

Mistake 3: Starting your SIP before you have this fund. Financial influencers love saying “start investing early.” That advice assumes you already have a financial buffer. Without an emergency fund, one bad month forces you to pause or withdraw your SIP — which means you’re repeatedly disrupting your long-term wealth-building. The emergency fund comes first. Always.

Mistake 4: Setting the target once and forgetting it. Your expenses in 2021 are not your expenses in 2026. If your rent has gone up, if you had a child, if you bought a car with an EMI, your emergency fund target has changed too. Review the number once a year — it takes five minutes — and top it up if needed.

Myth: “My Employee Provident Fund is my emergency fund.” This is perhaps the most common misconception among salaried professionals in India. EPF withdrawal for non-retirement reasons involves paperwork, EPFO portal delays (sometimes weeks), and tax deduction if withdrawn before five years of service. It is designed for retirement, not emergencies. Do not count it as part of your emergency buffer.

Also Read : What is CPSE ETF? Strength of India’s Public Enterprises

Frequently Asked Questions

What is the ideal emergency fund size for a salaried person in India?

For most salaried individuals in India, three to four months of actual monthly expenses is a solid starting target. If you are a sole earner, work in an unstable industry, or are self-employed, aim for six months. Always calculate based on your real monthly costs — rent, EMIs, groceries, utilities, and insurance — not your take-home salary, which overstates what you actually need to survive.

Where should I keep my emergency fund in India?

The most practical approach is a split strategy. Keep one to two months of expenses in a high-interest savings account — IDFC First Bank or AU Small Finance Bank offer 6–7% and allow instant access via UPI. Park the remaining amount in a liquid mutual fund through platforms like Groww or Zerodha Coin, where redemptions typically settle by the next business day at returns of 6.5–7.5%.

Can I use a fixed deposit as an emergency fund in India?

A regular fixed deposit is not ideal because breaking it prematurely attracts a penalty of 0.5–1% and requires manual action — time you may not have during a crisis. A sweep-in FD is a much better option. It automatically breaks in parts when your account balance drops below a set threshold, giving you instant access with no penalty. Most major private banks in India offer this feature.

How long does it realistically take to build an emergency fund?

With a consistent monthly contribution and any windfalls redirected here, most people in India reach a three-month emergency fund within 8 to 12 months. The key is automating the transfer on your salary credit date so it happens before you have a chance to spend. Start with whatever you can afford — even ₹1,500 a month — and increase the amount with every salary hike.

Should I start mutual fund SIPs before I have an emergency fund?

No. Build your emergency fund first. If you start investing without a financial buffer, any unexpected expense — a medical bill, job loss, home repair — will force you to pause or redeem your SIP at the worst possible time, often when markets are down. The emergency fund is what protects your investments and allows your SIPs to keep running through difficult periods.

Financial & Data Analytics Specialist | Investigations & Research | NCFM Certified | Editor | Investment Analyst | Finance Blogger | Writer | Over 15+ years of experience, turning complex money matters into clear insights. Through my writing, I help readers navigate wealth, markets, and financial trends with confidence.