Last Updated on 2 months ago by The Executive post

You earn a decent salary. By the 25th, you’re not sure where it went. Sound familiar?

Most Indians who struggle with money aren’t bad at earning — they’re bad at watching where it goes. A Deloitte study found that nearly 60% of urban Indian millennials run out of money before their next salary credit. The problem isn’t income. It’s visibility.

Expense tracking gives you that visibility. By the end of this article, you’ll know exactly how expense tracking works, which free apps are genuinely worth using in India in 2026, how to set one up in under ten minutes, and the mistakes that stop most people from ever sticking with it. No spreadsheets required.

Table of Contents

Why Track Expenses in India Is Different From the Rest of the World

Most expense tracking advice online is written for Americans or Europeans. They swipe credit cards for everything, so their bank app automatically categorises spending. Life in India works differently, and that changes everything.

Think about your own week: you might pay the sabziwala in cash, split dinner via GPay, pay rent by NEFT, and swipe your credit card for the gym. Indians juggle UPI, cash, cards, and wallets — often all in the same week. No single bank account captures your full financial picture, and that makes tracking harder.

This is why generic budgeting apps built for Western markets often fail Indian users. They connect to a bank account and show you card transactions — but they miss half your spending entirely. An app that cannot read your UPI transactions or your SMS alerts is not useful in the Indian context.

Income adds another twist. Many Indian households don’t have a neat monthly salary cycle. Freelance gigs, rental income, side businesses, Diwali bonuses, even agricultural earnings — money flows in irregular bursts. A simple salary-in, expenses-out model doesn’t reflect how families here actually manage cash. And when income is unpredictable, having an Emergency Fund is not just smart, it’s survival. It cushions you against delayed payments, medical surprises, or lean months when work slows down.

So what does a good expense tracker for India look like? It must read SMS alerts from banks and payment apps, allow manual entry for cash spending, and let you categorise expenses in ways that make sense for Indian life — groceries, EMIs, school fees, festival expenses, and yes, contributions to your Emergency Fund.

Once you see expense tracking through this lens, choosing the right app becomes much simpler — it’s about fitting the tool to your reality, not the other way around.

Best Free Expenses Tracking App in India in 2026

| App | UPI / SMS Sync | Manual Entry | Budget Alerts | Best For |

| Walnut | Yes (SMS-based) | Yes | Yes | Salaried professionals |

| Money Manager | No | Yes (detailed) | Yes | Cash-heavy households |

| Fi Money | Yes (account-linked) | Limited | Yes | Young urban professionals |

| ETMONEY | Yes (SMS-based) | Yes | Basic | Investors + expense trackers |

| Spendee | No | Yes | Yes | Couples and families |

| Goodbudget | No | Yes (envelope method) | Yes | Budget-conscious households |

Walnut App remains the most practical choice for most salaried Indians in 2026. It reads your SMS alerts from banks, credit cards, and UPI apps — no manual login required, no bank account linking. Every time you spend, it auto-categorises the transaction from your SMS. It covers cash too, with a quick manual entry option. The app is free, well-maintained, and has been around long enough to have reliable data privacy practices.

Fi Money works differently — it is a neo-bank that also track expenses. You open a Federal Bank account through Fi, and all your spending through that account is automatically tracked with smart categorisation. If you’re open to switching your primary salary account, this is the slickest experience available right now.

ETMONEY is ideal if you’re also investing in mutual funds. It track expenses from SMS and handles your SIP investments in one place. The dual functionality makes it worth having even if you eventually choose another primary tracker.

Money Manager is the right pick if you deal heavily in cash — traders, small business owners, or anyone whose spending doesn’t show up on digital trails. It’s purely manual but extremely well-organised with clear category breakdowns and a daily entry habit that takes under two minutes.

For couples or families managing a shared budget, Spendee or Goodbudget let multiple users contribute to one shared expense log — useful when both spouses are spending from different accounts.

How to Set Up Expense Tracking App in India — A Step-by-Step Start

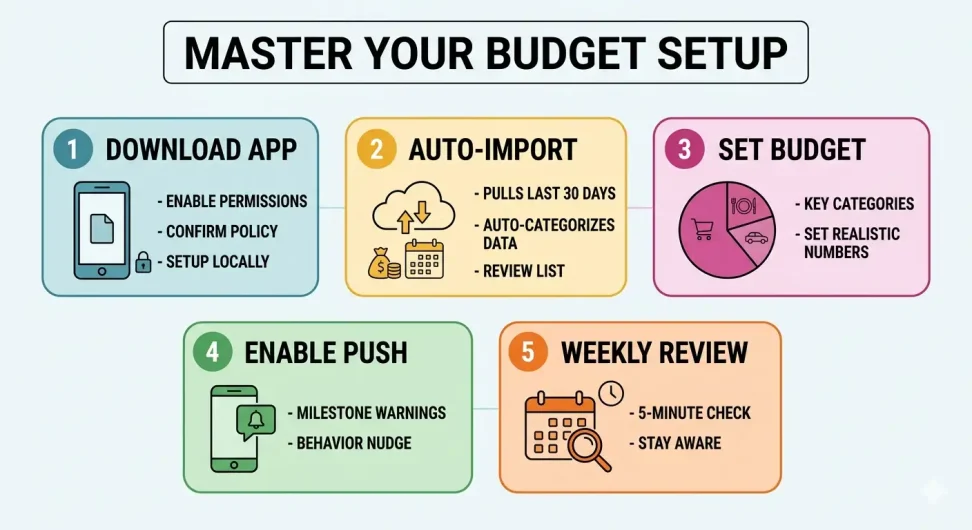

Knowing which app to keep track expenses to use is only half the job. Most people download a budgeting app, poke at it for three days, and abandon it. The setup phase is where most people fail. Here’s how to get it right the first time.

Step 1: Download Walnut (or your chosen app) and grant SMS permissions. Walnut needs access to your SMS inbox to read bank and UPI transaction alerts. This sounds alarming but is how the auto-sync works — the app reads locally on your phone and does not upload your SMS content to external servers. Take two minutes to read their privacy policy if you want to confirm this.

Step 2: Let the app import your last 30 days of transactions automatically. Walnut will pull your recent SMS-based transactions and categorise them. Go through this list once — it takes about five minutes — and correct any wrong categories. Your grocery order might be tagged as “Shopping.” Your EMI might show as “Transfer.” Fix these manually so the app learns your patterns.

Step 3: Set a monthly budget by category. Don’t try to budget everything in week one. Pick three categories that matter most: groceries, eating out, and entertainment. Set a realistic number for each — based on what you actually spent last month, not what you wish you’d spent. If you spent ₹8,000 eating out last month, set ₹7,500 as your target, not ₹3,000. Unrealistic budgets get abandoned immediately.

Step 4: Enable push notifications. Most good apps will alert you when you’re at 80% of a category budget. This is the feature that actually changes behaviour. You’re not reviewing a report once a month — you’re getting a nudge in real time. That changes decisions.

Step 5: Do a five-minute weekly review, not a monthly one. Monthly reviews feel like homework. A five-minute check every Sunday — what did I spend this week, what stands out — is enough to stay aware without feeling overwhelmed. Most apps have a weekly summary view for exactly this purpose.

A realistic timeline: expect to spend the first two weeks correcting categories and building the habit. By week three, the data starts to tell a real story about your spending. By month two, you will genuinely know where your money goes — probably for the first time.

Common Mistakes That Kill track Expenses Habits

Most people get this wrong in the same predictable ways. Here’s what to watch for.

Mistake 1: Trying to track expenses on every single rupee from day one. Perfectionism kills the habit faster than anything else. If you miss a ₹20 auto-rickshaw fare, that’s fine. What matters is getting 90% of your spending recorded consistently, not 100% perfectly.

Mistake 2: Using a separate app from where you actually pay. If you have to open a different app every time you spend money, you’ll stop doing it within a week. Choose an app that syncs automatically — like Walnut via SMS — so the tracking happens without you actively doing anything.

Mistake 3: Track Expenses on Tracking App but never reviewing. Data is only useful if you look at it. Downloading an app and letting it collect data you never check is the financial equivalent of buying a gym membership and never going. Schedule a five-minute Sunday review. Put it in your calendar.

Mistake 4: Setting budgets that punish rather than guide. If your current food budget is ₹12,000 and you try to cut it to ₹6,000 overnight, you’ll overspend by day ten and feel defeated. Reduce spending in 10–15% steps month by month. Small wins build long-term habits.

Myth: “I’ll just use a spreadsheet.” Spreadsheets work brilliantly — for people who actually use them every day. For most people, a spreadsheet starts as a promise and ends as a blank file sitting in Google Drive. A mobile app with SMS sync removes the friction entirely and actually gets used.

Conclusion

Three things to take away. Choose an app built for India — one that reads SMS alerts and handles UPI, cash, and card spending together. Set up in under ten minutes using the five-step process above — and fix your categories in the first two weeks. And review for five minutes every Sunday — that one habit will do more for your finances than any investment tip you’ve ever read.

One action for today: download Walnut, grant SMS access, and check what you spent in the last seven days. That number will surprise you — and that surprise is the first step to changing it.

Also Read : How to Invest in Nifty 50 Index Fund: A Complete Guide

Frequently Asked Questions

What is the best free Expense Tracking App in India in 2026?

Walnut app is the most practical free expense tracker for India in 2026 because it reads SMS alerts from banks and UPI apps automatically, so you don’t have to enter every transaction manually. For investors who also want to manage SIPs, ETMONEY is a strong alternative. For cash-heavy users or small business owners, Money Manager’s detailed manual entry system works better.

How do I track expenses in India if I use UPI and cash together?

The best approach is to use an SMS-based app like Walnut app, which captures all UPI and bank transactions automatically from your text alerts, and pair it with manual entries for cash spending. Take thirty seconds after each cash purchase to log it in the app. Over time, this two-source method gives you a complete picture of your spending that no single automated tool can provide on its own.

Is it safe to give an Expense Tracking App access to my SMS?

Reputable apps like Walnut App process your SMS data locally on your device — meaning they read the messages to extract transaction data but do not upload your SMS content to their servers. Always check the app’s privacy policy before granting access, look for apps with a long track record and large user base, and avoid granting SMS access to unknown or newly launched apps. Walnut app and ETMONEY have been operating in India for several years and have established privacy practices.

Can I track expenses for a family or couple in India using a free app?

Yes. Spendee and Goodbudget both allow shared budgets where multiple users can log expenses into one common tracker. This is particularly useful for couples managing a household budget from different bank accounts. Each person logs their own spending, and the app shows a combined view. Both apps have free tiers with enough features for most families.

How long does it take to see results from tracking your expenses in India?

Most people start noticing patterns within two to three weeks of consistent tracking — you’ll quickly identify where money is leaking, whether it’s food delivery, subscriptions, or impulse purchases. Meaningful behaviour change, where you actually start spending less in specific categories, typically happens between weeks four and eight. The key is doing a weekly review rather than waiting for a monthly summary, which keeps the data fresh and actionable.

Financial & Data Analytics Specialist | Investigations & Research | NCFM Certified | Editor | Investment Analyst | Finance Blogger | Writer | Over 15+ years of experience, turning complex money matters into clear insights. Through my writing, I help readers navigate wealth, markets, and financial trends with confidence.