Last Updated on 2 months ago by The Executive post

You put £500 into a “Best robo-advisors” three years ago. You barely touched it. Now you check and it’s grown — not because you did anything clever, but because an algorithm quietly rebalanced it while you slept. That’s the quiet power of robo-investing.

But here’s the thing: not all robo-advisors are built the same. In the UK, two names keep coming up — Nutmeg (now rebranded as J.P. Morgan Personal Investing) and Moneyfarm. Both promise hands-off, low-cost investing. Both are FCA-regulated. But the differences between them? They matter — especially to your wallet over 10 or 20 years.

By the end of this article, you will know exactly how these two platforms compare on fees, performance, account types, and who each one is actually right for.

Table of Contents

What Is a Robo-Advisor and Why Are UK Investors Using Them?

Let’s be honest — the word “robo-advisor” sounds more complicated than it is. Strip away the jargon and here is what you get: a digital platform that builds and manages an investment portfolio for you, automatically, based on your risk appetite and goals. No stock-picking. No spreadsheets. Just pick a risk level, put money in, and let it run.

These platforms typically invest your money in ETFs — Exchange-Traded Funds. Think of an ETF as a basket of hundreds of stocks or bonds packed into one simple product. Because you are buying the basket rather than individual shares, risk is spread out. And because it is mostly algorithm-driven, the management cost is far lower than hiring a human financial adviser.

In the UK, robo-advisors sit comfortably inside tax-efficient wrappers you probably already know — Stocks and Shares ISAs (up to £20,000 per year tax-free), SIPPs (personal pensions), and Junior ISAs for children. This makes them genuinely useful for long-term wealth building, not just speculation.

Adoption is growing fast. Rising costs of traditional advice, low savings rates, and a generation of younger professionals who are comfortable managing finances on an app have all pushed robo-advisors into the mainstream. If you have ever felt that “proper investing” was only for the wealthy or the finance-savvy robo-advisors were built specifically to prove that wrong.

Nutmeg vs Moneyfarm in 2026 — A Head-to-Head Comparison

First, an important update. Nutmeg, founded in 2012 and acquired by JPMorganChase in 2021, officially rebranded to J.P. Morgan Personal Investing UK in November 2025. The Nutmeg name is retired. If you open an account today, you are dealing with J.P. Morgan — though the underlying technology and investment approach remain largely the same.

Here is how they stack up:

| Feature | J.P. Morgan PI (formerly Nutmeg) | Moneyfarm |

| Minimum investment | £500 (£100 for LISA/JISA) | £500 |

| Management fee | 0.75% up to £100k; 0.35% above | 0.75% reducing to 0.35% above £500k |

| Fund costs (avg) | ~0.19% | ~0.20% |

| Portfolio options | 10 (fully managed) | 7 |

| Stocks & Shares ISA | Yes | Yes |

| SIPP (pension) | Yes | Yes |

| Lifetime ISA | Yes | No |

| Junior ISA | Yes | No |

| ESG portfolios | Yes | Yes |

| Human adviser access | Paid (restricted) | Free (via consultant) |

| FSCS protection | Yes (£120,000) | Yes (£85,000) |

A few things stand out here. J.P. Morgan Personal Investing is the only option if you want a Lifetime ISA — Moneyfarm does not offer one. That 25% government bonus for first-time buyers or retirement savers is substantial and worth factoring in if you are in the 18-39 age bracket.

On fees, they are closely matched at the lower end. However, Moneyfarm’s fee tiers drop more progressively as your portfolio grows — making it potentially cheaper for balances between £20,000 and £500,000. Performance data through 2023 showed J.P. Morgan (formerly Nutmeg) marginally ahead at the highest risk levels, with a £1,000 investment growing to around £1,549 over five years in its top-risk fully managed fund. Moneyfarm’s equivalent reached approximately £1,464 over the same period.

One standout with Moneyfarm is the free access to an investment consultant from £10,000 invested. For larger balances above £100,000, you get a qualified wealth manager included in the fee. J.P. Morgan Personal Investing does offer human advice, but it is a paid, restricted service — it only covers its own products.

What Should You Actually Do — Practical Steps to Get Started

Most people overthink this. Here is a simple, step-by-step approach depending on your situation.

If you are a first-time investor with under £10,000: Start with either platform — fees are equivalent at this level. Open a Stocks and Shares ISA, set a monthly direct debit (even £50 or £100 a month adds up), and pick a medium risk portfolio. Do not fixate on picking the “perfect” portfolio. Getting started matters more than getting it perfect.

If you want to buy your first home or save for retirement and you are under 40: J.P. Morgan Personal Investing is the only sensible choice here because of its Lifetime ISA. The government adds 25% on top of whatever you contribute, up to £4,000 per year — that is a free £1,000 annually. No other robo-advisor in this comparison offers this.

If you have between £20,000 and £100,000 to invest: Run the numbers. Moneyfarm’s tiered fees tend to be slightly cheaper in this range for managed portfolios. The free consultant access from £10,000 also adds real value — it is like getting light-touch financial advice baked into your annual cost.

If you want an ethical (ESG) portfolio: Both platforms offer it. ESG means your money avoids companies with poor records on environmental, social, and governance issues. Pick whichever platform suits your other needs.

One thing to check before you start: Both platforms are regulated by the FCA and covered by the FSCS. But note that the FSCS protection limit increased to £120,000 in December 2025 for J.P. Morgan Personal Investing, while Moneyfarm remains at £85,000. If your portfolio is growing toward that ceiling, it is worth knowing.

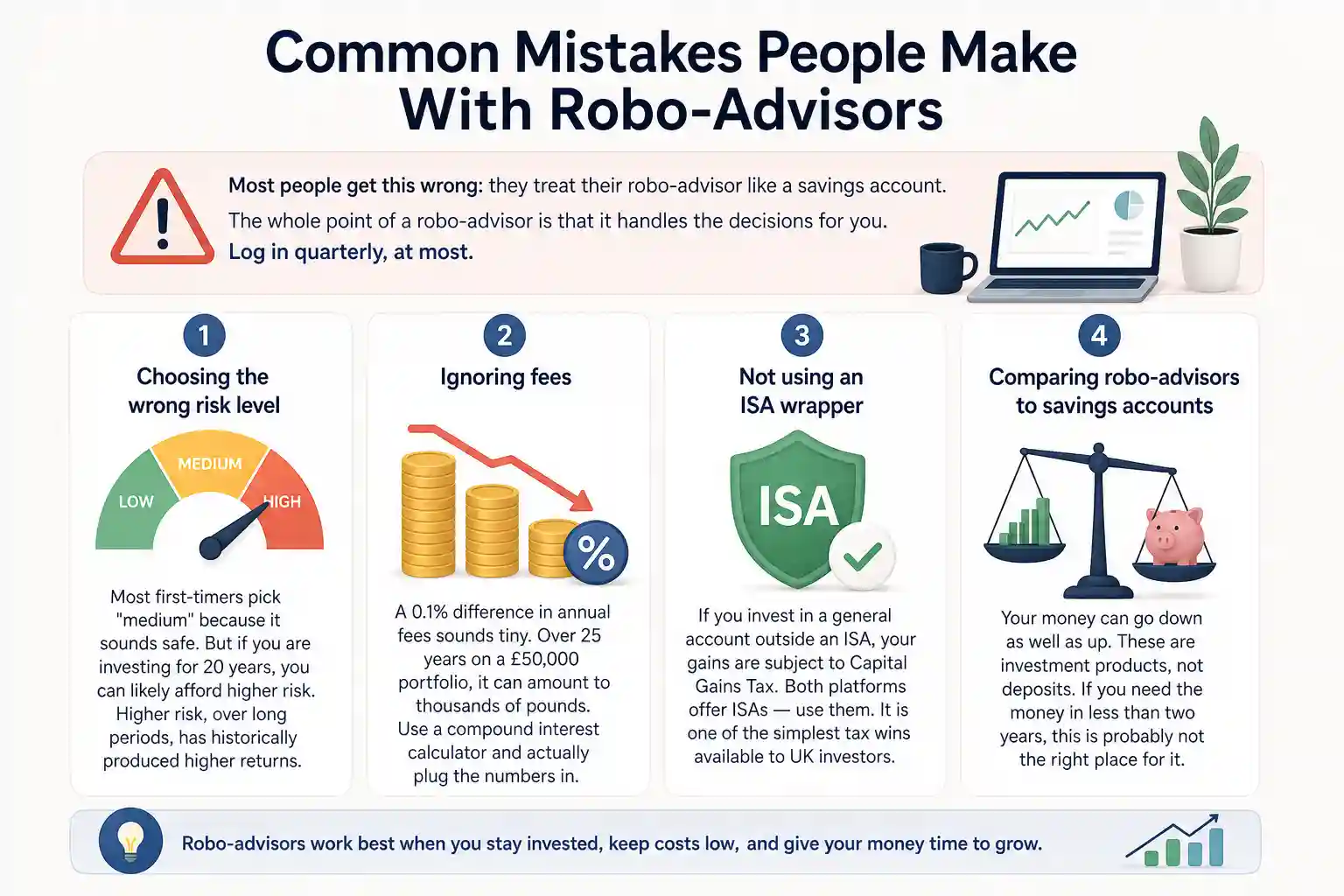

Common Mistakes People Make With Robo-Advisors

Most people get this wrong: they treat their robo-advisor like a savings account. Checking it daily, panicking when markets dip, moving to lower-risk portfolios at the worst possible moment — these habits destroy returns. The whole point of a robo-advisor is that it handles the decisions for you. Log in quarterly, at most.

Mistake 1 — Choosing the wrong risk level. Most first-timers pick “medium” because it sounds safe. But if you are investing for 20 years, you can likely afford higher risk. Higher risk, over long periods, has historically produced higher returns.

Mistake 2 — Ignoring fees. A 0.1% difference in annual fees sounds tiny. Over 25 years on a £50,000 portfolio, it can amount to thousands of pounds. Use a compound interest calculator and actually plug the numbers in.

Mistake 3 — Not using an ISA wrapper. If you invest in a general account outside an ISA, your gains are subject to Capital Gains Tax. Both platforms offer ISAs — use them. It is one of the simplest tax wins available to UK investors.

Mistake 4 — Comparing robo-advisors to savings accounts. Your money can go down as well as up. These are investment products, not deposits. If you need the money in less than two years, this is probably not the right place for it.

Myth worth busting: “Robo-advisors beat the market.” They almost never do. What they do well is provide broad, consistent exposure to global markets at low cost. That is not exciting — but it is genuinely useful for most people.

The Bottom Line — Which One Is Right for You?

Choose J.P. Morgan Personal Investing (formerly Nutmeg) if you want a Lifetime ISA, you value the J.P. Morgan brand and its research capabilities, or you want access to the widest range of account types under one roof.

Choose Moneyfarm if you have a growing portfolio over £20,000, you value free human guidance built into the fee, or you want a platform with a strong track record and progressively lower costs as your balance grows.

Both are solid. Both are FCA-regulated. Neither is a shortcut to getting rich. But compared to leaving money in a cash savings account earning below inflation, either one is a meaningful step forward.

Pick the one that fits your situation — and start this week, not next month.

Frequently Asked Questions (FAQ)

Is Nutmeg still available in the UK in 2026?

No — Nutmeg was officially rebranded as J.P. Morgan Personal Investing in November 2025, following its acquisition by JPMorganChase in 2021. All existing accounts migrated automatically; the core ETF-based investment approach remains unchanged.

Which is better JP Morgan Personal Investing UK (Nutmeg) or Moneyfarm?

Moneyfarm is cheaper for most portfolio sizes and includes free human consultant access, making it the stronger all-round pick. J.P. Morgan Personal Investing wins if you need a Lifetime ISA ,Moneyfarm does not offer one.

What are the best robo-advisors UK 2026 for beginners?

Both platforms are beginner-friendly — you answer a few questions, and the algorithm does the rest. Moneyfarm’s free investment consultant access gives it a slight edge for anyone who wants occasional human reassurance.

Are robo-advisors safe in the UK?

Yes — both are FCA-regulated and FSCS-protected, covering you up to £120,000 with J.P. Morgan Personal Investing and £85,000 with Moneyfarm if a platform fails. Note that FSCS does not protect against normal market losses.

How much do robo-advisors charge in the UK?

Both start at around 0.75% per year in management fees, dropping as your balance grows, plus roughly 0.20% in underlying fund costs. Total annual charges land around 0.90–0.95% for most investors — far cheaper than a traditional adviser.

Financial & Data Analytics Specialist | Investigations & Research | NCFM Certified | Editor | Investment Analyst | Finance Blogger | Writer | Over 15+ years of experience, turning complex money matters into clear insights. Through my writing, I help readers navigate wealth, markets, and financial trends with confidence.