Last Updated on 2 months ago by The Executive post

Nearly six out of ten working adults in the UK have money sitting in savings accounts that earn less than inflation, while a simple investment anyone can set up in under 20 minutes has quietly been building wealth for millions worldwide. That investment is an ETF and if you’ve ever wondered what is an ETF or how an ETF for UK investors really works, you’re not alone. By the end of this article, you’ll understand exactly how ETFs operate on UK platforms, which types suit different goals, how to make your first move without a financial degree, and the common mistakes beginners make that quietly cost money — plus how to sidestep every one of them.

Table of Contents

What Is an ETF for UK Investors — The Basics

ETF stands for Exchange-Traded Fund. Let’s break that down into plain English, because the name is doing a lot of work.

A fund is simply a pot of money pooled from many investors. That pooled money is then used to buy a collection of assets — shares in companies, government bonds, gold, or some combination of all three. Rather than you choosing individual stocks yourself, the fund holds them on your behalf.

“Exchange-traded” means the fund is listed and traded on a stock exchange — in the UK, that is typically the London Stock Exchange. You can buy and sell it during market hours, in real time, exactly as you would buy shares in a company like Lloyds or Unilever.

Here is the part that makes ETFs genuinely different from traditional managed funds. Most ETFs are passive. They do not employ a fund manager to pick stocks. Instead, they track an index — a pre-defined list of companies or assets. A FTSE 100 ETF, for example, simply holds shares in all 100 companies on the FTSE 100. When the index rises, your ETF rises. When it falls, so does your holding.

This mechanical simplicity keeps costs extremely low. And low costs, compounded over years, make an enormous difference to your final return. Global ETF assets crossed $14 trillion in 2025. In the UK, retail flows into ETFs have grown every single year for the past decade. There is a reason for that.

Types of ETFs UK Investors Should Know

Not all ETFs are the same. Choosing the right type matters more than most beginners realise.

Equity ETFs are the most widely held. They track indices filled with company shares — FTSE 100, S&P 500, MSCI World. They carry medium risk and are the most suitable starting point for most investors building long-term wealth.

Bond ETFs hold government or corporate bonds rather than shares. They tend to be less volatile, making them popular with investors who are closer to retirement or want to balance a higher-risk equity portfolio.

Commodity ETFs follow the price of physical goods — gold, silver, oil — without you needing to own the commodity itself. A gold ETF, for example, moves in line with the gold price.

Thematic ETFs concentrate on a specific trend or industry: artificial intelligence, electric vehicles, clean energy. The returns can be significant, but so can the losses if the theme falls out of favour.

| ETF Type | Risk Level | Typical Use Case |

| Equity (FTSE 100 / S&P 500) | Medium | Long-term wealth building |

| Bond | Low–Medium | Stability, retirement planning |

| Commodity (Gold, Oil) | Medium | Inflation hedge, diversification |

| Thematic (AI, EV, Tech) | High | Growth focus, higher risk tolerance |

One distinction worth knowing early: Physical ETFs actually purchase and hold the underlying assets. Synthetic ETFs use financial contracts to replicate performance without owning the assets directly. For anyone starting out, physical ETFs are simpler, more transparent, and the better default choice.

The three providers you will see most on UK platforms are Vanguard, iShares (by BlackRock), and Invesco.

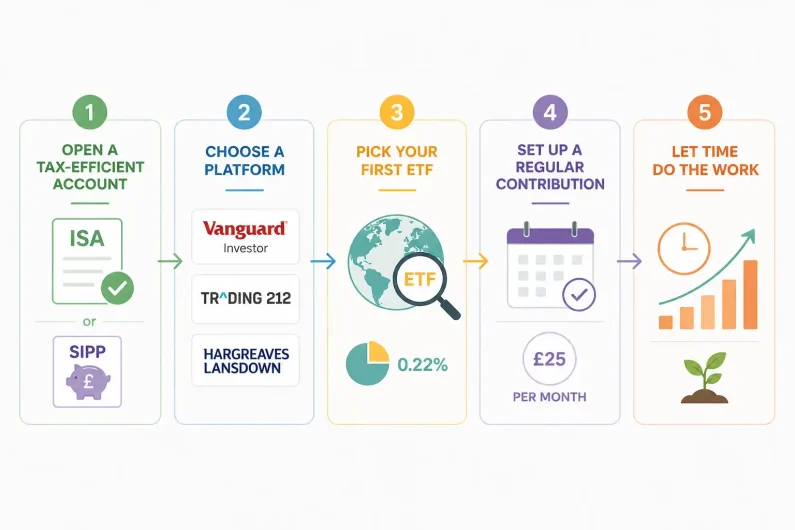

How to Start Investing in ETFs in the UK — Step by Step

This is where most guides go vague. “Just invest” is not a plan. Here is exactly what to do.

Step 1 — Open a tax-efficient account. In the UK, a Stocks and Shares ISA lets you invest up to £20,000 per tax year with no tax on gains or dividends. For most people, this is the right starting point. If you are investing specifically for retirement, a Self-Invested Personal Pension (SIPP) gives you tax relief on contributions — meaning the government tops up what you put in.

Step 2 — Choose a platform. Three names dominate the UK retail market:

- Vanguard Investor — ultra-low costs, ideal for simple ETF portfolios

- Trading 212 — commission-free trading, good for beginners

- Hargreaves Lansdown — wider choice, slightly higher fees but excellent tools

Step 3 — Pick your first ETF. If you are uncertain, start with one broad global equity ETF. The Vanguard FTSE All-World UCITS ETF (ticker: VWRL) holds over 3,500 companies across 50-plus countries. Its ongoing charge is 0.22% per year. On a £10,000 investment, that is roughly £22 annually in fees — a fraction of what an actively managed fund would cost.

Step 4 — Set up a regular contribution. Most platforms allow monthly investments from as little as £25. This approach is called pound-cost averaging — you buy more units when prices are low and fewer when they are high, which smooths your returns naturally over time.

Step 5 — Let time do the work. Review your portfolio once or twice a year. Do not check it daily. Patience, not activity, is what builds long-term wealth in ETF investing.

Common ETF Mistakes UK Beginners Make

Most errors in ETF investing are not about choosing the wrong fund. They are about behaviour and overlooked details.

Chasing thematic ETFs before building a foundation. AI, clean energy, and electric vehicle ETFs look exciting — and they can be. But concentrated themes mean higher volatility. Build a broad global or FTSE equity base first, then add thematic exposure if you want it.

Ignoring the ongoing charge figure. Every ETF has an annual fee expressed as a percentage. The gap between 0.07% and 0.75% sounds trivial. Over 25 years, on a £30,000 portfolio, it can mean a difference of tens of thousands in compounded returns. Always check the OCF before buying.

Skipping the ISA. Many new investors buy ETFs in a general investment account and later discover they owe Capital Gains Tax on profits above the annual allowance — currently £3,000 for the 2025–26 tax year. A Stocks and Shares ISA removes that liability entirely. Use it.

Selling during market falls. This is the single most costly mistake. When markets drop — and they will — the instinct is to sell and protect what remains. But selling locks in losses permanently. Investors who stayed invested through the 2020 crash recovered within months. Those who sold did not.

The discipline to hold when it feels uncomfortable is what separates investors who build wealth from those who merely try.

Avoiding these mistakes takes discipline, but technology can help. You may use ChatGPT for Personal Finance gives UK investors a practical edge: with the right prompts, you can simulate ETF scenarios, calculate the impact of fees, test ISA strategies, and even rehearse how to stay calm during market drops. Used alongside ETFs and robo-advisors, ChatGPT becomes a behavioral coach — helping you sidestep beginner errors, stay consistent, and grow wealth with confidence.

Conclusion

ETFs are one of the most accessible, cost-efficient tools available to UK investors today. Three points are worth carrying with you. First, an ETF gives you instant diversification — one purchase can spread your money across thousands of companies. Second, fees compound over decades, so keeping them low is one of the most impactful decisions you can make. Third, consistency and patience outperform timing and intuition every time. Increasingly, robo-advisors make this process even easier by automating ETF selection and portfolio management, ensuring beginners stay disciplined without needing deep financial expertise.

Your action for today: open a Stocks and Shares ISA on Vanguard Investor or Trading 212 and set up a £25 monthly contribution to a global ETF. That single step — whether managed directly or through a Robo-advisor — puts you ahead of most.

Frequently Asked Questions (FAQ)

What is an ETF for UK investors in simple terms?

An ETF is a fund that holds a basket of assets — shares, bonds, or commodities — and trades on a stock exchange like a regular share. UK investors can buy ETFs through platforms like Vanguard, Hargreaves Lansdown, or Trading 212, often starting with very small amounts. They are low-cost, transparent, and suitable for beginners and experienced investors alike. For most people, a broad global equity ETF is the simplest and most effective starting point.

Are ETFs a good investment for UK beginners in 2026?

ETFs are widely considered one of the best starting points for new investors because they spread risk across many holdings automatically. A single global ETF can give you exposure to thousands of companies without requiring you to pick stocks. The costs are low, the process is straightforward, and you do not need a financial adviser to get started. That said, all investments carry risk and values can fall as well as rise.

How are ETFs taxed in the UK?

ETFs held inside a Stocks and Shares ISA are completely tax-free — no Capital Gains Tax, no Income Tax on dividends. Outside an ISA, gains above the £3,000 annual CGT allowance are taxable, and dividends above the £500 allowance may attract Income Tax. Using your full ISA allowance before investing in a general account is almost always the more tax-efficient approach.

What is the minimum amount needed to invest in an ETF in the UK?

Many UK platforms, including Trading 212 and InvestEngine, allow you to start with as little as £1 through fractional investing — meaning you buy a portion of an ETF unit rather than a whole one. Vanguard Investor starts from £100 as a lump sum or £25 per month on a regular savings plan. There is genuinely no reason to wait until you have a large sum to begin.

What is the difference between an ETF and a mutual fund in the UK?

Both are pooled investment vehicles, but there are two key differences. ETFs trade on an exchange throughout the day at real-time prices, while mutual funds are priced once daily after the market closes. ETFs are also typically passive and cheaper — most charge under 0.25% annually — whereas many UK mutual funds charge 0.75% or more for active management that frequently underperforms the index anyway.

Financial & Data Analytics Specialist | Investigations & Research | NCFM Certified | Editor | Investment Analyst | Finance Blogger | Writer | Over 15+ years of experience, turning complex money matters into clear insights. Through my writing, I help readers navigate wealth, markets, and financial trends with confidence.